What Do I Do When My Financial Adviser Can’t Cope

What Do I Do When My Financial Adviser Can’t Cope The financial press have seen what appears to be an increasing number of articles on financial advisory firms that have been having service issues, typically caused by the departure of financial advice and administration staff. As someone who understands the financial services profession, I gather […]

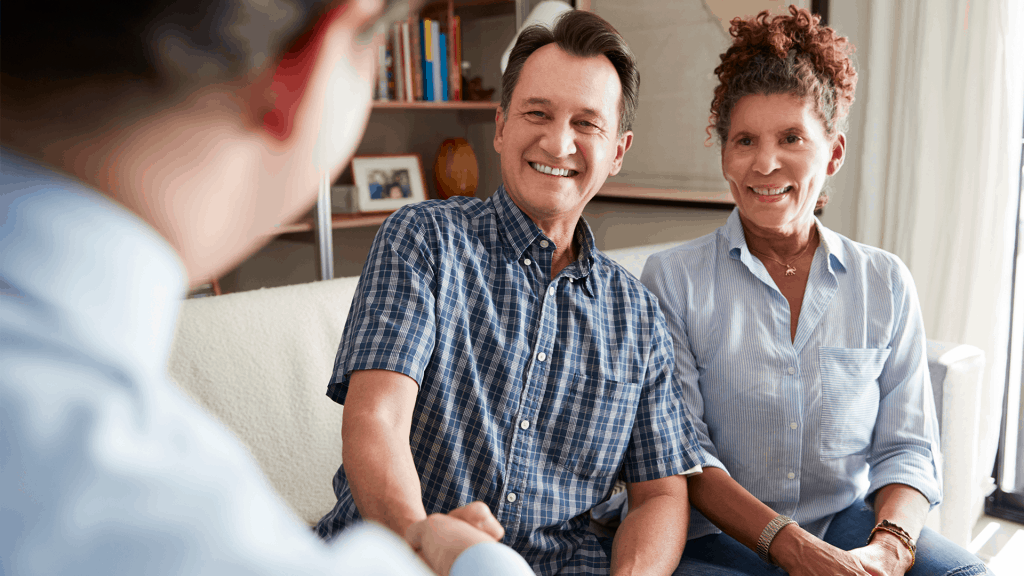

Top tips to help you get the most from your financial adviser

Top tips to help you get the most from your financial adviser You have made the decision to engage with a financial adviser and ideally, you only want to make the choice of which financial adviser just the once. It is therefore important to make sure you get the most from your chosen financial adviser. […]

Pension Death Benefits for Vulnerable Beneficiaries

Pension Death Benefits for Vulnerable Beneficiaries The pension freedoms that were introduced in April 2015 improved the death benefits on pensions. For the first time it was possible for individuals to nominate that their pension fund would pass to anyone on death, rather than to dependants only which had chiefly been the case before 2015. […]

An increase to self-employed national insurance? Be careful what you wish for!

The Chancellor’s budget makes provision for a £360m cost for the abolition of Class 2 National Insurance Contributions (NICs) from 2018; with the self-employed moving to the same single tier state pension as employed individuals. Although the phasing out of Basic and Second State Pensions is a total con for most people in the UK, the […]

Deferred payment agreements introduced by The Care Act 2014

Since April 2015, deferred payment agreements have been available from all councils across England that enables people to use the value of their homes to help pay care home costs. Subject to eligibility, the local council will help to pay your care home bills on your behalf. This option allows the delay of repaying the […]

2016.04: April Economic Review

UK Highlights GDP growth 0.60% Quarter on Quarter growth 2015 Q4 CPI inflation has been recorded at 0.30% in February 2016 For November 2015 to January 2016, 74.1% of people aged from 16 to 64 were in work, the highest employment rate since comparable records began in 1971. The unemployment rate for November 2015 to […]

What’s better, a workplace pension or a Lifetime ISA?

For most people, a workplace pension where an employer offers a matching contribution is likely to be better. There are some ‘soft’ benefits of a Lifetime ISA (LISA), for example the availability of early access with penalties, but looking at the tax position, the options speak for themselves. LISA Pension (BRT) Pension(HRT) Pension + Matching (BRT) […]

2016-17 Allowances at a glance

Income Tax Allowances Personal allowance £11,000 Dividend allowance £5,000 Savings rate band £5,000 Personal savings allowance £1,000 (£500 for higher rate tax payers, £0 for additional) Income tax bands and rates Effective rate Dividend rate Basic rate band £11,000 – £43,000 20% 7.5% Higher rate band I £43,000 – £150,000 40% 32.5% Loss of personal allowance […]

The pensions lifetime allowance should be a target, not a limit

The Lifetime Allowance (LTA) is the most tax efficient sum that can be accrued in a pension pot without further tax charges. For Money Purchase arrangements, and for lump sums from Final Salary Schemes it is simply the pound note value of benefits that are assessed, with Defined Benefits and other scheme pensions being assessed as 20x the pension payable.