UK Highlights

- GDP growth 0.40% Quarter 3 (July to Sept) 2015

- CPI inflation has been recorded at 0.20% in December 2015

- For September to November 2015, 74.0% of people aged from 16 to 64 were in work, the highest employment rate since comparable records began in 1971.

- The unemployment rate for September to November 2015 was 5.1%, down from 5.8% for a year earlier.

- Comparing September to November 2015 with June to August 2015, the number of people in employment increased by 267,000 (to reach 31.39 million), the number of unemployed people fell by 99,000 (to reach 1.68 million) and the number of people aged from 16 to 64 not in the labour force (economically inactive) fell by 93,000 (to reach 8.92 million

- Year-on-year estimates of the quantity bought in the retail industry showed growth for the 32nd consecutive month in December 2015, increasing by 2.6% compared with December 2014.

Source: Office for National Statistics

Developed Markets

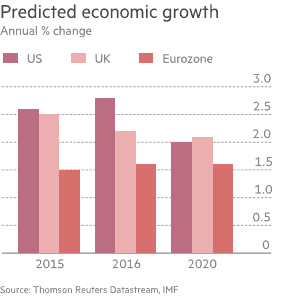

The US is expected by the International Monetary Fund to be the fastest growing advanced economy over the next few years.

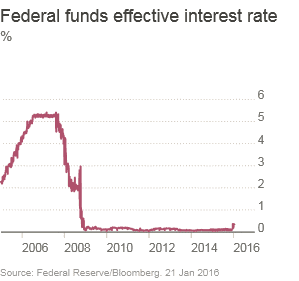

The US has seen recruiting in the private sector for a sustained period and unemployment has halved since its peak. With concerns that the jobs market could spur a pick-up in inflation and wages, the Federal Reserve has for the first time in nearly a decade increased the cost of borrowing to keep inflation low and the economy on an even keel.

Rates have been at rock-bottom levels since the financial crisis. While they are starting to rise, on the Federal Reserve’s own projections they will not return to pre-crisis levels in the foreseeable future. The effective rate is the average of what banks are actually paying each other, hence the fluctuations in the graph

In the Eurozone including the UK Interest Rates remain on hold.

Global

With recent downward revisions to Q4 GDP forecasts in a number of leading economies, 2015 is now set to record the slowest pace of global growth this cycle at 3.1%. Consensus forecasts show an improvement for 2016 but with world output predicted to be only a few tenths stronger at 3.3%. Both developed and emerging economies are projected to contribute driven by private sector demand-led growth in the euro area and Japan, an improvement in Russia and a rebound in numerous Asian economies

Oil prices have continued to fall and this does filter through to consumers who have more spending capacity as a result. At Regional level, those producing are hardest hit whilst those importing achieve a benefit of lower costs. The ongoing decline in commodity prices continues to create very challenging conditions for a number of the resource-based countries in Emerging Markets such as Brazil, Russia and South Africa. In particular, the former has wide-ranging economic and political problems set to plague the country for some time yet.

Investment Review

As I began to write this article the global stock-markets had already began 2016 in negative territory, sparked by the events in China. This week alone, we have seen the UK FTSE 100 index enter ‘Bear Market’ territory – a fall of 20% from its peak in April 2015. As we end the week the Market has rebounded strongly and we advise clients to ride out the volatility and remain focused on the longer term. It appears that the usual events that trigger Bear Markets, such as economic recession, unemployment becoming high or inflation rising, are not happening in the UK. For these reasons, we believe that investors should not panic.

Performance of major asset classes year to date

| Asset class | Growth / % |

| High yield bonds | 1.2 |

| Global government bonds | 5.8 |

| Cash | 0 |

| UK government bonds | 3 |

| UK corporate bonds | 1.1 |

| Index-linked bonds | 3.2 |

| US shares | -5.9 |

| Asian (ex Japan) shares | -10.4 |

| Emerging market shares | -9.9 |

| UK shares | -9.3 |

| European shares | -7.8 |

| Japanese shares | -7.1 |

Source: Morningstar Direct. Returns rebased in sterling for period 01/01/2016 – 20/01/2016.

What are the implications for investors? At Wingate, we believe it is going to be difficult to predict what happens in the short term. But we continue to believe in the principle of diversification across asset classes, regions and investment managers. We hope the following points help;

- Very few, if any of Wingate’s clients hold 100% equity portfolios – therefore when markets fall, the headlines reported are not their own experiences or falls in valuations.

- Falls only turn into losses if you sell out

- It is impossible to time markets successfully, which is proved yet again by recent research. A decision to sell followed by a second decision about when to buy back in, a very hard call to make.

- Have faith in the efficiency of a well-diversified balanced portfolio.